¿Planea retirarse? El dinero (equity) acumulado en su casa puede ayudarle a alcanzar su objetivo

¿Planea retirarse? El dinero (equity) acumulado en su casa puede ayudarle a alcanzar su objetivo “Baby Boomers“, Demografía, Para los vendedores, Mercado de la tercera edad Ya sea que se haya jubilado o esté pensando en la jubilación, es posible que esté considerando sus opciones y tratando de imaginar una etapa completamente nueva de su vida. Y no está solo. La investigación de la Asociación de Fideicomisos de la Industria de la Jubilación (Retirement Industry Trust Association – RITA por sus siglas en inglés) muestra que 10,000 Baby Boomers alcanzan la edad típica de jubilación (65 años) cada día, y solo el 47 % de las personas en esa generación ya se han jubilado. Si esto suena familiar, una cosa que vale la pena considerar es si su casa actual se adaptará o no a su nuevo estilo de vida. Si su casa no tiene las características o beneficios que está buscando, la buena noticia es que puede estar en una mejor posición para mudarse de lo que cree. Esto se debe a que, si ya es dueño de una casa, es probable que haya acumulado una plusvalía significativa, y eso puede ayudarle a impulsar su próxima mudanza. Según la Asociación Nacional de Realtors (NAR por sus siglas en inglés): “Un propietario que compró una casa típica hace cinco años habría ganado $125,300 solo con la apreciación del precio”. De hecho, en los últimos doce meses, CoreLogic informa que el propietario promedio en los Estados Unidos ganó aproximadamente $64,000 en plusvalía debido a la apreciación del precio de la casa. Usted puede usar su capital para ayudarle a alcanzar sus metas de la propiedad de la vivienda. Ya sea que desee reducir el tamaño, acercarse a sus seres queridos o comprar una casa en un destino de ensueño, su plusvalía puede ayudarle a llegar allí. Puede ser parte (si no todo) lo que necesitaría como pago inicial en una casa que se adapte mejor a sus necesidades cambiantes. Para averiguar cuánta plusvalía tiene en su casa, comuníquese hoy con un profesional en bienes raíces de confianza. En conclusión, La jubilación es un gran paso y también lo es comprar o vender una casa. A medida que avanza hacia esta nueva fase de la vida, vamos a comunicarnos para que tenga un experto que le guie a través del proceso a medida que venda su casa actual y brindarle asesoramiento experto al comprar una que se adapte mejor a sus necesidades.

Read More

What Would a Recession Mean for the Housing Market?

What Would a Recession Mean for the Housing Market? According to a recent survey from the Wall Street Journal, the percentage of economists who believe we’ll see a recession in the next 12 months is growing. When surveyed in July 2021, only 12% of economists consulted thought there’d be a recession by now. But this July, when polled, 49% believe we will see a recession in the coming 12 months. And as more recession talk fills the air, one concern many people have is: should I delay my homeownership plans if there’s a recession? Here’s a look at historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession would mean for the housing market today. A Recession Doesn’t Mean Falling Home Prices To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at the recessions going all the way back to 1980, home prices appreciated in four of the last six recessions. So, historically, when the economy slows down, it doesn’t mean home values will fall. Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would repeat what happened then. But this housing market isn’t about to crash. The fundamentals are very different today than they were in 2008. So, don’t assume we’re heading down the same path. A Recession Means Falling Mortgage Rates Research also helps paint the picture of how a recession could impact the cost of financing a home. As the chart below shows, historically, each time the economy slowed down, mortgage rates decreased. Fortune explains that mortgage rates typically fall during an economic slowdown: “Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.” And while history doesn’t always repeat itself, we can learn from and find comfort in the historical data. Bottom Line There’s no doubt everyone remembers what happened in the housing market in 2008. But you don’t need to fear the word recession if you’re planning to buy or sell a home. According to historical data, in most recessions, home price gains have stayed strong, and mortgage rates have declined. If you’re thinking about buying or selling a home, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Read More

Planning To Retire? Your Equity Can Help You Reach Your Goal.

Planning To Retire? Your Equity Can Help You Reach Your Goal. Whether you’ve just retired or you’re thinking about retirement, you may be considering your options and trying to picture a whole new stage of your life. And you’re not alone. Research from the Retirement Industry Trust Association (RITA) shows that 10,000 Baby Boomers reach the typical retirement age (65) every day, and only 47% of the people in that generation have already retired. If this sounds like you, one thing worth considering is whether or not your current home will suit your new lifestyle. If your home doesn’t have the features or benefits you’re looking for, the good news is, that you may be in a better position to move than you realize. That’s because, if you already own a home, you’ve likely built-up significant equity, and that can help you fuel your next move. According to the National Association of Realtors (NAR): “A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.” In fact, over the last twelve months, CoreLogic reports the average homeowner in the United States gained roughly $64,000 in equity due to home price appreciation. You can use your equity to help you achieve your homeownership goals. Whether you want to downsize, move closer to loved ones, or buy a home in a dream destination, your equity can help get you there. It may be some (if not all) of what you’d need as your down payment on a home that better fits your changing needs. To find out how much equity to have in your home, reach out to a trusted real estate professional today. Bottom Line Retirement is a big step and so is buying or selling a home. As you move into this new phase of life, let's connect so you have an expert to guide you through the process as you sell your current home and give you expert advice as you buy one that’ll better suit your needs.

Read More

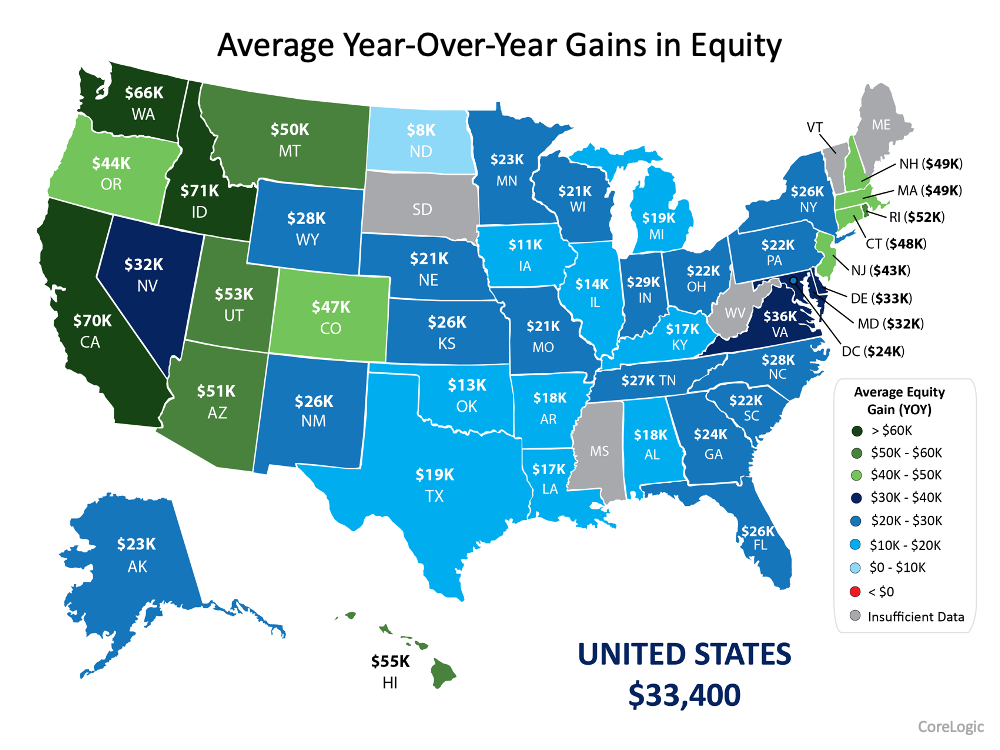

Homeowner Wealth Increases Through Growing Equity This Year

Building financial wealth and stability remains one of the top reasons Americans choose to own a home, and as a homeowner, your wealth often grows without you even realizing it. In a recent paper published by the Urban Institute, Home Ownership is Affordable Housing, author Mike Loftin illustrates how homeowners increase their equity and their wealth simply by making monthly mortgage payments: “The principal portion that reduces the loan balance builds the homeowner’s equity. In doing so, the principal payments behave like an automatic savings account. The principal payment is not money going out; it is money staying in.” But home equity – the difference between the value of your home and what you currently owe – isn’t just built through your monthly principal payments. Home price appreciation plays a vital role in growing your equity and, ultimately, your wealth. As Freddie Mac explains: “Homeownership has cemented its role as part of the American Dream, providing families with a place that is their own and an avenue for building wealth over time. This ‘wealth’ is built, in large part, through the creation of equity…Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability.” Homeowners Continue To See Equity Increase CoreLogic recently published its latest Homeowner Equity Insights Report, and it shows continued growth in equity amidst record home price appreciation. The report provides several key takeaways, all of which point to rising wealth for homeowners: The average equity gain of mortgaged homes during the past year was $33,400 The current average equity of mortgaged homes is greater than $216,000 There was a 6% increase in total homeowner equity over the past year Total U.S. homeowner equity has reached nearly $1.9 trillion Here, you can see the equity gains by state: Equity Provides Homeowners with Flexibility In addition to being a critical tool in building wealth, a homeowner’s equity also provides significant flexibility. When you sell your house, the accumulated equity comes back to you in the sale. Recent increases in home equity coupled with record-low mortgage rates mean it could be the perfect time for homeowners looking to make a move. Mark Fleming, Chief Economist at First American, notes: “Existing homeowners today are sitting on record amounts of equity. As homeowners gain equity in their homes, the temptation grows to list their current home for sale and use the equity to purchase a larger or more attractive home.” Increasing equity also helps families facing challenges brought on by the pandemic. Frank Martell, President, and CEO of CoreLogic, explains in the recent Homeowner Equity Insights Report: “Homeowner equity has more than doubled over the past decade and become a crucial buffer for many weathering the challenges of the pandemic. These gains have become an important financial tool and boosted consumer confidence in the U.S. housing market, especially for older homeowners and baby boomers who’ve experienced years of price appreciation.” Bottom Line Home equity has always been a powerful wealth-building tool, and homeowners continue to see their financial stability increase. Let’s connect today so you can better understand how much equity you have in your current home or if you’re ready to take the next step in building your savings as a homeowner.

Read More

Categories